Key takeaways

- Annual house price inflation slows to 5.3%, down from 8.6% last year

- Buyer demand and sales volumes are 20-50% lower than a year ago but slightly ahead of the pre-pandemic years (2017-2019)

- Sellers having to accept an average 4.5% discount to the asking price to achieve a sale –the highest for 5 years as a buyers’ market takes hold

- Average discount to asking price is £14,000 meaning sellers are having to forgo a third of their pandemic house price gains

- Broad based repricing of housing is underway with UK house price inflation set to move into low negative year-on-year by summer

- Market is still on track for a soft landing with modest price falls of up to 5% and 1 million sales in 2023

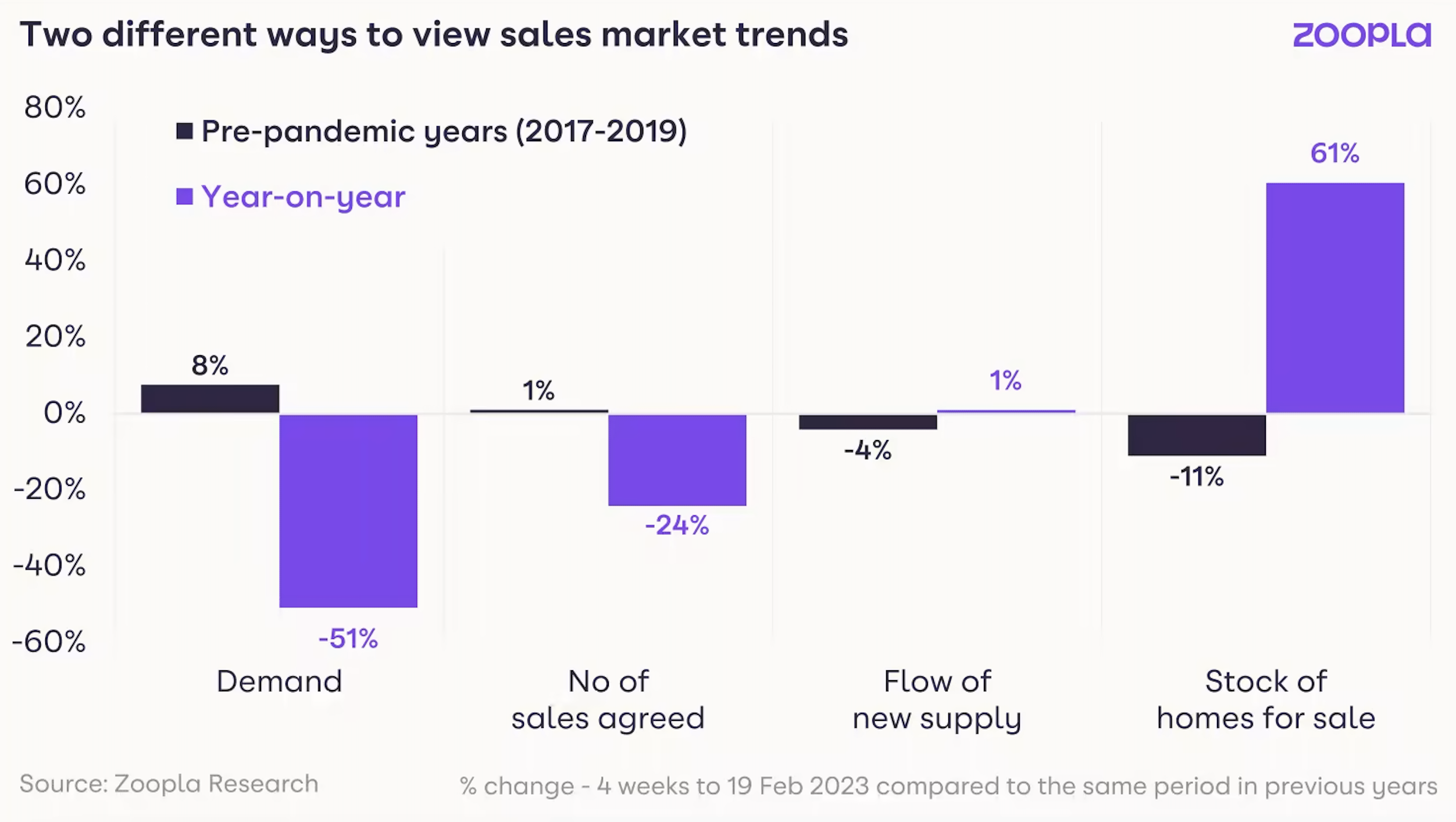

Glass half-full or half-empty?

It is possible to take two opposing views on performance in the current sales market. The glass-half-empty view is to look at trends on a year-on-year basis, comparing this year to the red-hot market conditions a year ago.

The glass-half-full view compares the current market to the pre-pandemic years (2017-2019) when activity levels and house price growth were more benign and trading conditions were tougher.

Year-on-year comparisons are important for businesses benchmarking how they are faring compared to last year. Our data shows demand from home buyers has rebounded in the first two months of 2023 but remains at half the level recorded a year ago.

New sales volumes in early 2023 have also recovered, tracking the usual seasonal upturn we see each year, albeit 24% lower than this time last year.

The reality is that current market conditions are more aligned with the pre-pandemic years with demand 8% higher and sales agreed up 1%.

This is the more useful benchmark for businesses as they plan strategies and investment decisions now the frothy market conditions of the pandemic years are well and truly behind us.

Activity levels holding up in more affordable markets

While overall sales volumes are lower year-on-year, they are ahead of the pre-pandemic years in more affordable housing markets such as the North East and Scotland.

This is because higher mortgage rates have less of an impact on demand in lower-value markets. In contrast, sales volumes in the Midlands and southern England are up to 9% lower compared to the pre-pandemic period.

Higher house prices, which have grown fast over the last 2 years, mean a greater impact on buying power and levels of demand from would-be buyers. Sales are 4% above their pre-2020 levels in London. In this far-from affordable market, house prices and market activity have significantly underperformed the rest of the country since 2016. This makes the capital appear better value for money, which is supporting sales.

Asking to achieved price gap widens to largest for 5 years

While sales volumes have recovered, sellers are having to accept larger discounts to the asking price to secure sales. Negotiating down from the asking price was normal practice before the pandemic boom in England, Wales and Northern Ireland. In Scotland, most homes are marketed as ‘offers over’.

The latest data from valuation and risk business Hometrack shows that the discount to achieve a sale has increased over the last 5 months and currently stands at 4.5% - an average £14,100 discount per sale.

Discounts to asking price are larger than in the pre-pandemic years and reflect the rapid transition from a hot sellers' market - where most buyers had to pay the asking price over much of 2021 and 2022 - to a buyers' market with more negotiation on price.

Putting this discount into context, the average UK home grew in value by £42,000 over the pandemic, suggesting sellers are having to forgo, on average, 33% of their pandemic gains to achieve a sale.

Soft reset in house prices underway

The transition to a buyers’ market is being accompanied by nationwide repricing as the market adjusts to the reduction in buying power resulting from higher mortgage rates.

Buying power is starting to recover as mortgage rates fall from their 6% highs of late 2022.

Even at 4% mortgage rates, the average home buyer has 20% less buying power than they did a year ago when mortgage rates were 2%.

This will not feed straight through into house prices. Some buyers will look to buy smaller or cheaper homes as we highlighted last month. Others may inject more equity into purchases or be in position to spend more on mortgage repayments.

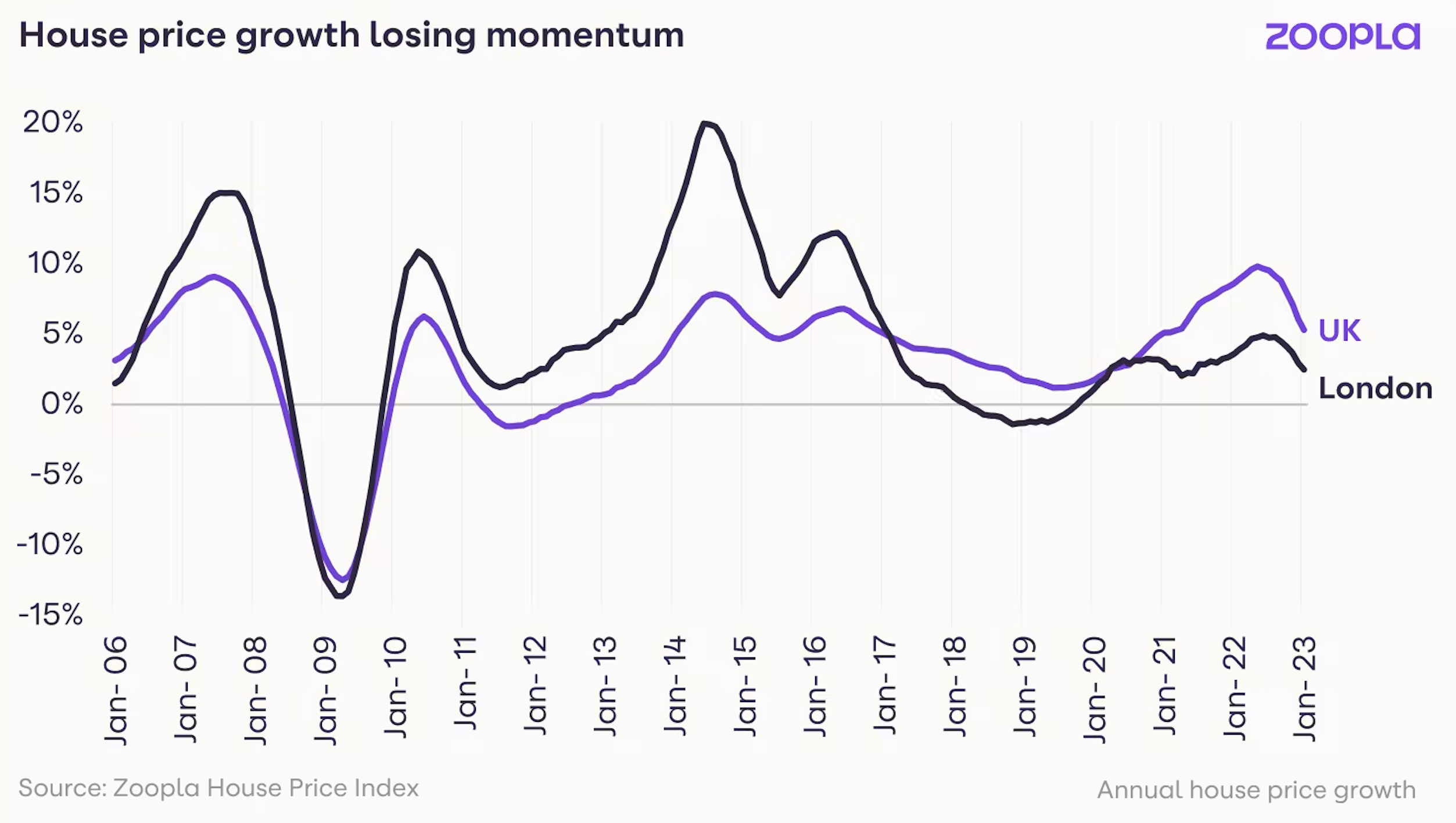

House price indices have started to pick up the decline in agreed prices over recent months. Our House Price Index is now registering modest monthly price reductions which have dragged the annual rate of inflation lower to 5.3%.

We expect our UK index to continue to show small month-on-month price reductions over the next 2-4 months as a soft reset in house prices continues. By the summer, we anticipate our index to be recording modest annual price reductions of up to 2 or 3%.

On a regional basis, the annual growth rate ranges from +2.5% in London to +7.1% in Wales.

The real weakness in price inflation is coming through southern England where high house prices compound the impact of higher mortgage rates on buyers.

Our index continues to show above-average house price growth in affordable regional towns next to larger employment centres covering postal areas such as Oldham, Dudley, Wolverhampton and Worcester where price inflation remains over 8%.

Inner London areas continue to top the list with the weakest rates of annual price growth although no postal areas are registering year-on-year price falls at this stage.

Outlook for the housing market in 2023

The housing market is adjusting to higher mortgage rates better than many had feared and it’s welcome news to see more rates for new buyers now in the 4-5% range and even lower.

Mortgage rates are unlikely to get much cheaper but competition among lenders will remain strong and keep deals attractive for borrowers.

Our view has always been that 4% mortgage rates are manageable and consistent with very low levels of house price growth or price falls in real terms.

It is welcome to see evidence of greater realism from sellers on pricing to secure a sale. The gains made over the last 2 years provide a buffer that can be used to unlock sales and it appears that this adjustment in pricing is uniform across the market by area and property type.

All this points to reasonable levels of turnover in 2023 which will support business plans for agents, builders and lenders. The industry can manage modest price falls so long as the impetus to move remains.

Working from home, increased retirement, and high immigration all continue to stimulate demand to move home. Cost-of-living pressures exacerbate those needs for some. If the market delivers 1 million to 1.1 million sales in 2023, as we expect, then it will be a positive result.

Source: Zoopla